In March 2017, the Enagás Board of Directors agreed to join the Code of Good Tax Practises. This Code, promoted by the Tax Agency, contains recommendations to improve the application of the tax system in corporations through increased legal certainty, reciprocal cooperation based on good faith and legitimate trust between the Tax Agency and companies, and the implementation of responsible fiscal policies in companies with the knowledge of the Board of Directors.

Enagás’ tax policy was approved by the Board of Directors on May 22, 2017, and establishes the strategy and principles that must guide the conduct of all Enagás professionals, as well as its value chain or third parties with which the company has dealings.

Furthermore, in line with its commitment to fiscal transparency, Enagás voluntarily submits an annual Fiscal Transparency Report (following approval by the Board of Directors), which is in line with the principles and good practices adopted by Enagás in its Tax Policy and the other fiscal governance measures approved by the Board.

In June 2022, the company received the t*** seal, the highest category in the ranking prepared by the Haz Foundation, which accredits IBEX35 companies with the highest standards in terms of transparency and fiscal responsibility.

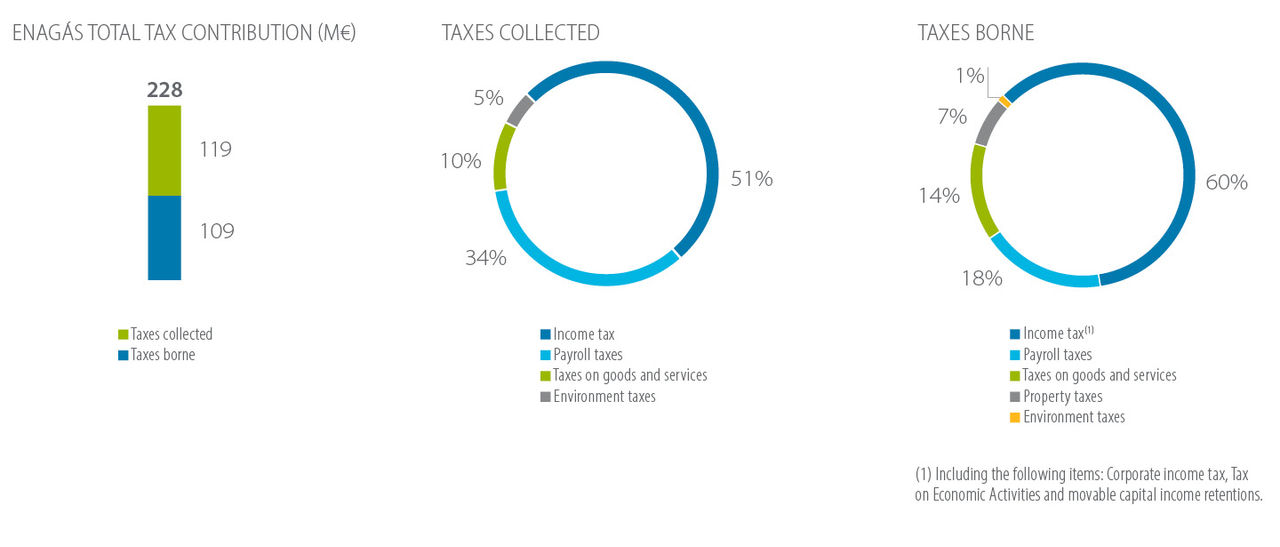

Enagás publishes in its Annual Report the calculation of its Total Tax Contribution (TTC). This methodology measures the impact represented by the payment of taxes by Enagás from the point of view of the total contribution of taxes paid directly to the Public Administration as a result of the company’s economic activity.

The additional contribution from domestic and international equity accounted affiliates is 125 million euros. Taxes borne total 82 million euros and taxes collected are 43 million euros.

They are those taxes that the company has paid to the tax authorities of the different countries in which it operates. These taxes are the ones that have been a real cost for Enagás, such as, for example, corporate income tax and environmental taxes.

They are those taxes levied on behalf of other taxpayers as a result of the economic activity of Enagás, without incurring any costs other than those of its administration.

The following is a breakdown of Enagás’ tax contribution in the 2022 Country by Country Report, which includes the tax jurisdictions of Spain, Mexico, Peru, the United States and Chile, which are fully and proportionally consolidated companies.

| Jurisdiction | Average number of employees | Foreign intercompany | Domestic third parties | Foreign third parties | Profit before corporate income tax | Corporate Income Tax paid (cash basis) | Corporate income tax accrued in the current year * | Tangible assets other than cash and cash-equivalent instruments | |||||||||||

| Germany | Belgium | Colombia | France | Greece | Italy | Morocco | Mexico | Norway | Peru | United Kingdom | Switzerland | ||||||||

| Spain | 1,373 | 0 | 965,811,047 | 40,832 | 343,568 | 42,099 | 182,230 | 830,135 | 125,431 | 70,895 | 95,883 | 28,288 | 747,790 | 176,480 | 293,457 | 285,356,290 | 92,961,539 | 79,966,677 | 4,217,213,146 |

| Mexico | 2 | 0 | 111,599 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | -1,000,837 | 0 | 7,919 | 145,473 |

| Peru | 3 | 0 | 828,507 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | -186,624 | 6,654 | 4,118 | 358,592 |

| USA | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | -9,598,663 | 0 | 1,398,241 | 0 |

| Chile | 1 | 0 | 579,976 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 237,294,626 | 0 | 68,610,667 | 0 |

* In Spain, the existing increase in the effective rate vs. the nominal rate is mainly due to the limitation of the dividend exemption to 95%. In the other jurisdictions (Mexico, Peru, United States and Chile), this difference is due to i) their status as holding companies, with exempt income (dividends); or ii) companies with an immaterial level of income. Taxation in these jurisdictions is carried out through equity-accounted affiliates, the details of which are not included in this scope.

With regard to tax havens, and in accordance with the provisions of its Tax Policy, Enagás does not use opaque structures to reduce its tax burden, nor does it carry out artificial operations not linked to its business activity to reduce taxation.

Likewise, the company does not make any investments in or through territories qualified as tax havens according to prevailing Spanish tax regulations, for the purpose of reducing the tax burden. Enagás does not currently have a presence or carry out any activities in territories classified as tax havens in accordance with Order HFP/115/2023, of February 9, 2023, which determines the countries and territories, as well as harmful tax regimes, that are considered non-cooperative jurisdictions.

/